In this video update, Todd from Integrity Investment Advisors emphasizes that market volatility is inevitable and drawdowns of 10% to 25% are completely normal aspects of long-term investing. This should be expected rather than feared. To weather these fluctuations, he recommends a customized “three-bucket” portfolio strategy consisting of a safety bucket using bonds for near-term cash flow, an alternatives bucket for hedging, and a long-term equity bucket to outpace inflation and drive compounding growth. Because rapid algorithmic trading makes market timing nearly impossible, investors are encouraged to consistently invest rather than wait on the sidelines. In fact, historical data shows that market dips offer excellent opportunities to invest more for strong forward returns, and counterintuitively, buying at all-time highs often produces even better future results due to positive market momentum. Ultimately, by leveraging the firm’s newly enhanced back-office capabilities and adhering to a disciplined Investment Policy Statement, investors can ignore short-term noise, capitalize on corporate earnings growth, and confidently achieve their financial goals.

If you want to work on your personal financial plan or want a 2nd opinion about your strategy & red flags, please schedule a meeting

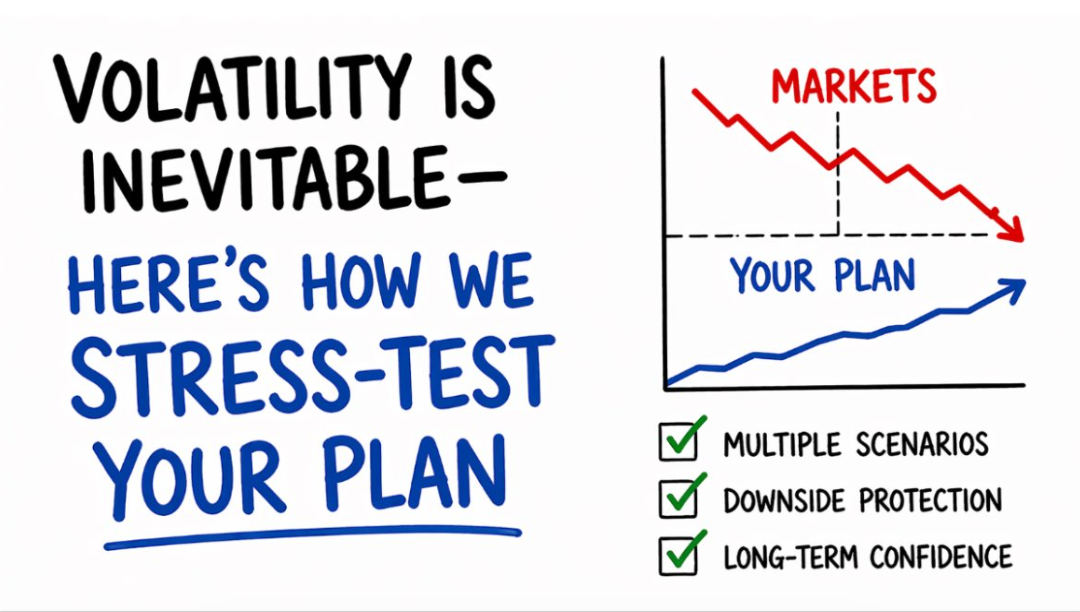

5 Key Points:

1. Volatility is a normal part of long-term investing. It is common for markets to experience drawdowns of 10% to 25% in any given year, and this volatility is simply the price you pay for long-term market gains. Investors should stay grounded, as betting against the market is usually a losing strategy. Markets go up 75% of the time over a one-year period and 95% of the time over a seven-year period.

2. Buying at all-time highs often yields better returns. Counterintuitively, historical data from 1989 onward shows that investing when the market is at an all-time high actually leads to better forward returns than buying on any average day. This is because strong market momentum and positive sentiment often lead to multiple all-time highs stacking up over 1-, 3-, and 5-year periods.

3. Market drops are prime opportunities for growth. When the market drops by 10%, 15%, or 20%, it is an ideal time to rebalance your portfolio and put more money to work. Historically, forward returns after a 10% market drop are very strong, averaging a 15% return over the following year and a 72% return over a five-year period.

4. Portfolios should use a “three-bucket” strategy. To balance risk and return, portfolios should be divided into three buckets. A “safety bucket” of defensive assets (like fixed income or bonds) should be used to cover four to five years of near-term spending. This allows the “long-term equity bucket” to freely grow and outpace inflation, while an “alternatives bucket” provides hedging and risk mitigation.

5. Financial planning and consistent investing beat market timing. Because market drops and their subsequent recoveries happen incredibly fast due to algorithmic trading, attempting to time the market is ineffective. Instead, investors should focus on stress-testing their portfolios, following an updated Investment Policy Statement (IPS), and consistently investing every few weeks or months to successfully build wealth over the long haul.

Frequently Asked Questions

Should I worry about recent market volatility?

Market volatility and drawdowns of 10% to 25% in any given year are completely normal. In fact, volatility is simply the price you pay for long-term investing. While markets can go down very quickly, they often go back up very quickly as well. Over time, betting against the markets is a minority view, as they go up 75% of the time over one-year periods and 95% of the time over seven-year periods.

Is it a bad idea to invest when the market is at an all-time high?

Surprisingly, no. Buying at all-time highs actually tends to yield better forward returns than buying on any other day. This is due to positive market momentum and sentiment, which can lead to many all-time highs stacking up in a single year. Watch the video for more details.

What should I do when the market experiences a significant drop?

When the market goes down 10%, 15%, or 20%, it is a good opportunity to put more money to work and rebalance your portfolio. Forward returns after drawdowns are historically very strong; for instance, after a 10% drop, forward returns average 15% over the next year and 72% over a five-year period. If market drops happen too quickly to manually act on, consistently buying every two weeks or every month is a great long-term strategy.

How should I structure my portfolio to protect myself while still growing my wealth?

- Safety bucket: Used for liability matching, this holds safer assets (like fixed income) to cover 4 to 5 years’ worth of spending needs.

- Alternatives bucket: Used for hedging and risk mitigation, this diversifying bucket helps portfolios weather tough markets.

- Long-term equity bucket: Used for growth. Even if you are retired, you must maintain growth assets in your portfolio to outpace inflation and compound your wealth over the coming decades.

If you want to work on your personal financial plan or want a 2nd opinion about your strategy & red flags, please schedule a meeting

- Why Diversification Matters in 2026: Navigating the 2026 Market 2/19/2026

- Are we in an AI/Tech Bubble 11/5/2025

- Markets are Looking Forward: Recovery From April Lows 8/4/25

- A Roadmap to Succeed in Pullbacks & Recessions 4/5/25

- There is always something to worry about 3/12/2025

- How much risk do you need to take to hit your goals? 11/5/2024

- Is it normal for stocks to go down -5% to -10% in a short period of time? 8/7/24

- Are Things Getting Better or Worse? 3/27/24

- Market Recap & Path Forward 2024 -1/16/24

- Markets Normally Go Up & Bear Markets Are Transitory – 7/16/23

- Stocks are up 11% per year for the last 7 years! 6/30/22

- The Answer to Volatility is Financial Planning 5/6/2022

- Tough Choices — What do we own & why? 2/17/2022

- Are Things Getting Better or Worse? 10/15/2021

- Back to Normal but Now What? 5/7/21

Thanks for reading/watching. This website is for educational purposes only and is not investment advice.

Benchmark Performance Reports Disclosures:

Historical performance results for investment indexes, ETFs, mutual funds and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing historical performance results. None of the indexes, ETF or mutual funds are meant to describe the performance of actual clients. They are only for informational & educational purposes. The S&P 500 is not the only index used as a benchmark for measuring the performance of a portfolio. Depending upon the holdings in your portfolio, your investment objectives, and your risk tolerance, it may be more appropriate to measure performance against a different benchmark like MSCI World, balanced portfolios or bonds. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark or index strategy.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended by the advisor), will be profitable or equal to past performance levels. All investment strategies have the potential to profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client’s investment portfolio.

The information provided herein is for informational purposes only and is not intended to be, and should not be construed as, legal or tax advice. You should consult with a qualified tax advisor, CPA, or attorney before making any decisions based on this material, as individual situations may vary. We do not provide tax or legal advice. Any tax strategies discussed are general in nature and may not be appropriate for your specific circumstances.

Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Integrity Investment Advisors’ website and its associated links offer news, commentary, and generalized research, are not personalized investment advice. Nothing on this website should be interpreted to state or imply that past performance is an indication of future performance. All investments involve risk and unless otherwise stated and are not guaranteed. Be sure to consult with a tax professional before implementing any investment strategy. Investment Advisory Services offered through Integrity Investment Advisors, a Registered Investment Adviser with the U.S. Securities & Exchange Commission. Registration does not imply a certain level of skill or training.

Subscribe To Our Blog! We helpClients retire without getting killed in taxes!

Free tools & Checklists! Your Retirement will thank you!

Free & valuable information to help you maintain your lifestyle in retirement. We cover Vanguard indexing, DFA and factor investing (value, small cap, high profit, momentum). Free tools & market insights.

See why you may need a low-cost, fee only Advisor who is a fiduciary for you 100% of the time.

You have successfully subscribed. Thank you! Here are some free resources - Video - A note from your future self - https://youtu.be/HKMYTLyhOGU 5 Free Checklists That May Save You Thousands – Really! Countless people need help in these areas. Checklists include: end of year tax planning, funding a child's college education, caring for aging parents, items to consider before you retire, critical documents to keep on file. Please like & share with family & friends. You can download the PDFs for free. https://www.integrityia.com/5-free-checklists-that-may-save-you-thousands-really/